There are many versions of this old saying shared by Presidents Harry S. Truman and Ronald Regan but the sentiment is the same. “It’s a recession when your neighbor loses her job; it’s a depression when you lose your own.” Virtually no industry has been spared from this horrific worldwide Covid-19 pandemic. There are a few that have done well, some have stayed neutral while the vast majority and especially small businesses have been devastated and the alcohol industry is no exception. Some of the larger firms have done fine in certain segments but overall the outlook is not good.

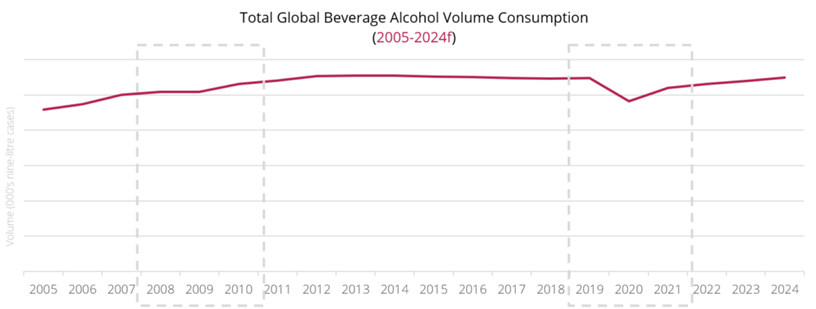

According to new research from IWSR Drinks Market Analysis it’s going to take years for the beverage alcohol market to recover. Though worldwide beverage alcohol volume increased slightly in 2019, reversing declines from the year prior IWSR says it will be five years before the global industry rebounds from the ongoing Covid-19 crisis.

Total global alcohol consumption, led by increases in beer and ready-to-drink products, grew by +0.1% in volume and +3.6% in value in 2019, but losses in the months-long near complete shutdown of bars and restaurants across the world this year has not been offset by upticks in liquor retail and ecommerce. IWSR expects this to lead to double-digit declines in 2020, which IWSR estimates will take until 2024 to reach 2019 pre-Covid-19 levels (though in the UK and US, IWSR forecasts that pre-Covid-19 beverage alcohol volume levels likely won’t return until after 2024.) Global travel retail, severely affected by widespread travel restrictions, will see a particularly harsh decline in 2020 but is expected to reach pre-crisis levels by 2024.

Covid-19 Pandemic More Severe Than the 2008 Downturn

“While we’re still assessing the full impact of the current Covid-19 situation, it’s very clear that the pandemic is set to cause a deeper and more long-lasting after-effect to the global drinks industry than anything we’ve experienced before. Even the downturn following the 2008 financial crisis was less severe than what we are seeing now,” says Mark Meek, CEO of IWSR Drinks Market Analysis, the leading authority on the global beverage alcohol market. “In many ways, 2019 was perhaps the last ‘normal’ year for the drinks industry.”

Beer Expected to Rebound Better than Wine and Spirits

Globally, beer (not including flavored malt beverages like hard seltzers) grew 0.3% in volume and +2.2% in value in 2019, led particularly by increases in non-alcoholic beer (+15.2% in volume, vs. 2018). Though the beer category has taken a hit in 2020, the outlook for continued growth of no-alcohol beer remains positive, with a forecasted +8.1% CAGR 2019-2024. In total, beer is expected to reach 2019 volumes by 2024, rebounding better than wine and spirits.

Increasingly Less Tied to Celebratory Moments, Sparkling Wine Outshines Still Wine

The long-term global decreases in wine consumption continued in 2019, posting a -1.1% volume decline (though value was slightly up, at +0.6%). In the key consuming region of North West Europe, wine volumes have been slowing at a rate of -1.6% CAGR 2014-2019, and in the US, wine consumption last year declined for the first time in 25 years. One bright spot in the category, however, is sparkling wine which posted growth of +1.4% volume, and +3.6% value in 2019, and is forecasted to rebound stronger than still wine by 2024, as consumers increasingly shift to year-round consumption of these products.

Spirits Drop -2.5% in 2019; Whisky and Gin on Pace to Recover Fastest

Overall, total spirits dropped -2.5% in volume last year, due in part to steep volume losses in baijiu (a spirit consumed almost entirely in China). Excluding baijiu, however, global spirits volume grew +1.0% in 2019.

No-Alchohol Spirits Saw Highest Percentage Growth

No-alcohol spirits were the fastest-growing spirits segment by volume in 2019, +25.5%, though still small in terms of market share (and of note, 2018-2019 was the first period that IWSR began tracking the no-alcohol spirits category). Amongst traditional spirits categories, gin was the fastest growing in 2019 (+6.1%), but that growth has slowed somewhat as consumers are beginning to show signs of “gin fatigue,” especially in some European markets (growth of gin globally was +9.6% in 2018). Within the whisky category, Irish grew by +10.6% volume, Japanese increased +10.3%, and US whiskey posted +5.8%. The IWSR forecasts that whisky and gin will likely rebound fastest to pre-Covid-19 levels. Vodka volumes are not expected to recover to 2019 levels until after 2024.

Ready-to-Drink & Hard Seltzers Poised for Continued Growth

For the third consecutive year, ready-to-drink (RTD) products in 2019 were the fastest growing beverage alcohol category, up +19.6% in volume and +18.8% in value. Even though RTDs only represent a small slice of beverage alcohol market share, they contributed more than double the value growth to the industry than wine in 2019. Much of this interest and growth in the category is fueled by the innovation and convenience of hard seltzers in the US, which last year grew by over +200% in volume. The global RTD category is forecasted to grow by +7.2% volume CAGR 2019-2024.

Stay Informed: Sign up here for the Distillery Trail free email newsletter and be the first to get all the latest news, trends, job listings and events in your inbox.

Beverage Alcohol Ecommerce Holds Huge Opportunities

Beverage alcohol ecommerce posted gains last year, which should be welcome news to brands battling current challenges brought by Covid-19. Across 16 key markets studied by the IWSR, all beverage alcohol categories in 2019 grew in value faster online versus the total market.

- Beer ecommerce value grew +14% (vs +1% growth for the total market value)

- Wine grew +18% (vs. total market decline of -1%)

- Spirits grew +15% (vs. total market growth of +6%)

Based on an ecommerce study published last year by IWSR, the value of the channel at the time was US$21bn (across 10 core markets), which is almost twice that of global travel retail, pre-Covid-19.

“As restrictions ease, long term recovery is expected to be slower than the initial bounce back – driving a ‘Nike Swoosh’ rebound shape,” adds Meek. “Like many other industries, it’s incredible how a few months of lockdown will result in several years of recovery, but beverage alcohol has proven to be remarkably resilient in previous downturns, and this should be no different. A strong focus on innovation, premiumization, and new routes to market such as ecommerce, are all factors which will help contribute to the industry’s rebound and future growth.”

Please help to support Distillery Trail. Sign up for our Newsletter, like us on Facebook and follow us on Instagram and Twitter.